The Takeaway

In the second quarter of 2026, the Federal Reserve held the federal‑funds rate steady amid persistent inflation, leaving leveraged loans sensitive to movements in credit spreads rather than base rates.

In the second quarter of 2026, the Federal Reserve held the federal‑funds rate steady amid persistent inflation, leaving leveraged loans sensitive to movements in credit spreads rather than base rates.

The Bank of England maintained the Bank Rate at 3.75% at its June 2026 meeting, giving policymakers time to assess how the energy shock is propagating through the UK economy before committing to further action. The European Central Bank raised the key ECB rates to 2.25% in June in response to inflationary pressures.

The Bank of England maintained the Bank Rate at 3.75% at its June 2026 meeting, giving policymakers time to assess how the energy shock is propagating through the UK economy before committing to further action. The European Central Bank raised the key ECB rates to 2.25% in June in response to inflationary pressures.

Second-quarter 2026 Treasury yields moved higher across the curve, led by the intermediate segment, where yields between two and seven years rose by an average of approximately 30 basis points. Longer-dated yields increased more modestly, resulting in a flatter yield curve as persistent inflation concerns and a cautious Federal Reserve stance kept upward pressure on front-end and belly rates.

Second-quarter 2026 Treasury yields moved higher across the curve, led by the intermediate segment, where yields between two and seven years rose by an average of approximately 30 basis points. Longer-dated yields increased more modestly, resulting in a flatter yield curve as persistent inflation concerns and a cautious Federal Reserve stance kept upward pressure on front-end and belly rates.

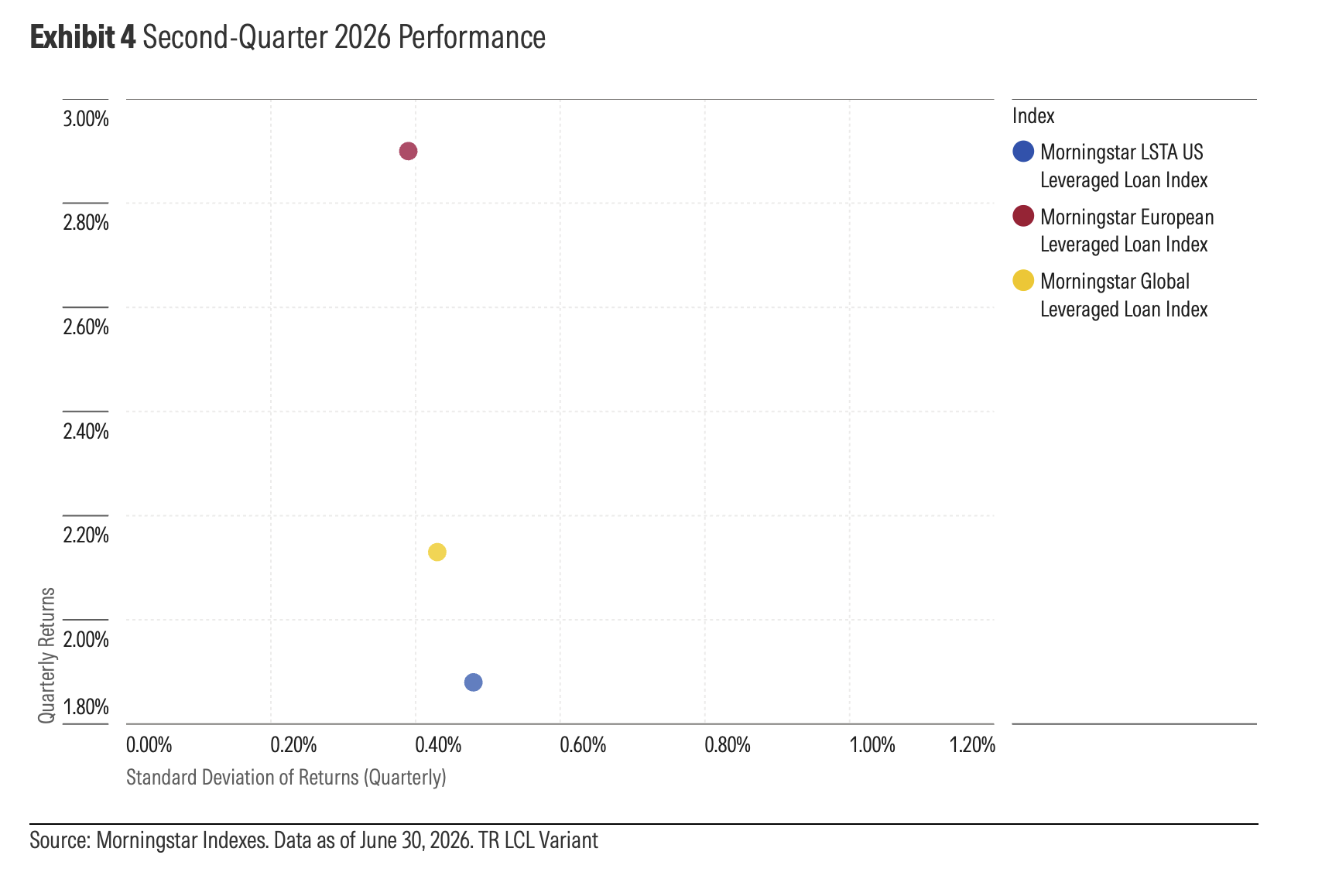

Declining spreads fueled a broad-based recovery across leveraged loans, resulting in positive returns during the quarter. The Morningstar European Leveraged Loan Index delivered the highest return at 2.90%, followed by the Morningstar Global Leveraged Loan Index at 2.13%, while the Morningstar LSTA US Leveraged Loan Index returned 1.88% in the second quarter.

Declining spreads fueled a broad-based recovery across leveraged loans, resulting in positive returns during the quarter. The Morningstar European Leveraged Loan Index delivered the highest return at 2.90%, followed by the Morningstar Global Leveraged Loan Index at 2.13%, while the Morningstar LSTA US Leveraged Loan Index returned 1.88% in the second quarter.

The Morningstar Leveraged Loan Monitor for Q2 2026 delivers an in-depth analysis of the leveraged loan market, with a focus on the US, European, and global indexes.

Market volatility eased relative to the first quarter of 2026, as spreads compressed broadly and secondary loan prices recovered, including a partial rebound in the previously beleaguered software sector in Europe. Against this backdrop, leveraged loans rebounded strongly during the quarter. The Morningstar European Leveraged Loan Index led with a return of 2.90%, followed by the Morningstar Global Leveraged Loan Index at 2.13%, while the Morningstar LSTA US Leveraged Loan Index returned 1.88%, held back by continued softness in US software credits. Issuance activity diverged by region, with US volumes slowing to USD 185 billion from USD 222 billion, while European issuance strengthened modestly to EUR 62 billion from EUR 60 billion, led by healthcare equipment and services.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.