The eyes of investors and the markets are on SpaceX, OpenAI and Anthropic as these prominent unicorns prepare to go public and enter market indexes that power some of the largest ETFs and mutual funds.

These three companies are part of a growing cohort coming to market with substantially larger market valuations than anything seen in the past. And these mega IPOs increasingly have lower relative free float (or shares available to the public). How major public market indexes treat these companies will be very important, according to Morningstar Indexes. A new paper entitled The Impact of Mega-IPOs on the CRSP Market Indexes addresses investor worries around these new IPOs and the potential impact on broad market indexes through the lens of the CRSP US Total Market Index.

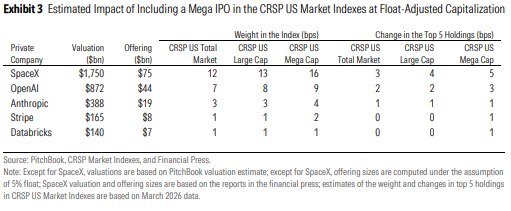

First on investor worry lists is the impact a very large private company like SpaceX may have on portfolios connected to market benchmarks at initial inclusion. Since new securities are added to the index at the level of shares that are publicly available to investors, or its free float, the initial inclusion impact is much more limited.

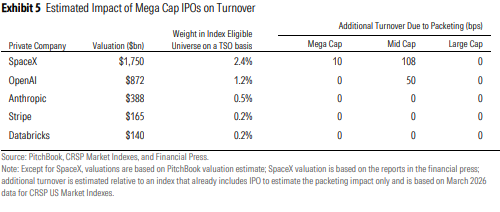

Second on investor worry lists is the impact of reconstitution, when indexes recalculate the relative rankings of all securities to determine their placement in market cap segments based on total shares outstanding. While some smaller companies may move from the CRSP Mega Cap Index to the CRSP Mid Cap Index at reconstitution with the addition of a large new IPO to the US Total Market Index, banding and packeting methodologies will minimize the level of turnover.

Alex Poukchanski – Director of Index Analytics, Morningstar:

“As companies continue to stay private longer and grow in valuation before considering going public, it is understandable that markets and investors are concerned about the potential impact these companies may have on broad market indexes and the ETFs and funds that track them. Thoughtful evolution of our index methodology to accommodate the changing markets, combined with our innovative packeting and transitional reconstitution rules, helps minimize these potential impacts while ensuring that our US equity indexes continue to provide an accurate picture of the total US equity opportunity set.”

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.