As you’ve probably heard, “mega IPOs” may soon hit the US stock market. SpaceX has reportedly filed confidentially for an initial public offering of $75 billion in stock, valuing the company at an astounding $1.75 trillion. Waiting in the wings are artificial intelligence companies—Anthropic, OpenAI, and Databricks. These IPOs are expected to dwarf previous blockbuster listings like Saudi Aramco 2222, Facebook (now Meta META), and Alibaba BABA.

To some, these upcoming IPOs represent a long-overdue broadening of access to private companies. To others, their rapid inclusion into indexes and the funds that track them amount to “jamming retail investors with an overpriced IPO.”

It’s important to keep these potential IPOs in perspective, though. While they will affect both private and public markets, the impact shouldn’t be overstated.

The Magnificent Seven Meets the Magnificent Few

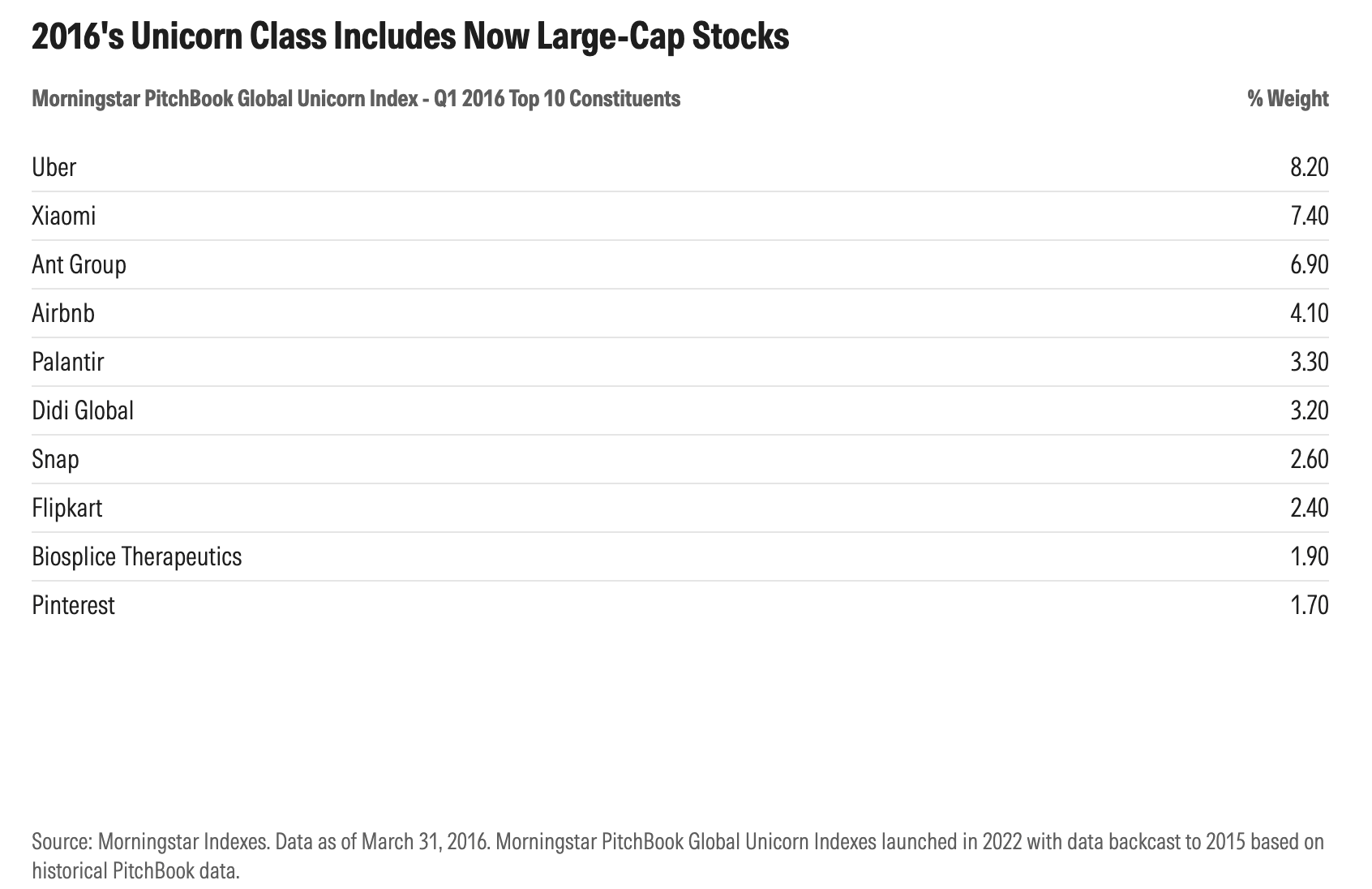

I wrote recently about rising concentration levels in the US stock market using 100 years of equity market data from the Center for Research in Security Prices. It turns out that private markets are even more concentrated, thanks mostly to SpaceX and the AI companies. The top 10 constituents for the Morningstar PitchBook Global Unicorn Index currently represent nearly 40% of the universe of venture-backed businesses valued at $1 billion or more. That’s even more top-heavy than the CRSP US Total Stock Market Index, which is dominated by Magnificent Seven companies: Nvidia NVDA, Apple AAPL, Alphabet GOOGL, Microsoft MSFT, Amazon.com AMZN, Meta META, and Tesla TSLA.

Yes, there are far fewer unicorns than public companies. But private companies worth more than $1 billion are no longer as rare as implied by the 2013-era term. The unicorn index currently contains 1,424 constituents (versus 3,477 for the CRSP US Total Market Index).

“The market has rarely exhibited this degree of sector-level concentration, reflecting AI’s unique potential and endless opportunities to be implemented across every sector,” wrote PitchBook analysts in a new research report called “The Magnificent Few.” Investment has flooded into “pre-IPO” companies. Not just venture capital, but also “crossover” investors have chased unicorns, including retail mutual funds with small portfolio allocations, some that have made huge bets, and other more questionable strategies.

Valuations for the Magnificent Few are staggering. As mentioned, SpaceX, which recently acquired xAI (also founded by Elon Musk), could IPO at a $1.75 trillion valuation. According to PitchBook, OpenAI may come to market at a valuation of $840 billion and Anthropic at $330 billion. By way of comparison, the largest IPO of 2025, Figma FIG, was valued at just $12 billion. Facebook was valued at roughly $104 billion at its 2012 IPO and Alibaba at roughly $168 billion in 2014.

What Will Mega-IPOs Mean for Private Markets?

PitchBook researchers who follow private markets worry that mega IPOs will crowd out other potential exits. Kyle Stanford, PitchBook’s Director of Venture Capital Research, wrote that “three companies might swallow the entire pie” of what was supposed to be a broad wave of public listings in 2026, referring to SpaceX, OpenAI, and Anthropic. If their performance as public companies underwhelms, that could deter others. Stanford also noted that venture capitalists won’t benefit from IPOs to the extent expected given how much non-traditional investment has flooded into private markets:

"SpaceX, OpenAI, and Anthropic are rumored to go public in 2026. Should that occur, they would likely be the three largest VC-backed IPOs ever and could conceivably create more value than all VC-backed IPOs since 2000 have collectively. This would be a win for VC, a market that has been stranded in a liquidity crunch for several years. However, these returns would be relatively concentrated, with large portions of value being held by corporates and non-VC investors." - Kyle Stanford

Exits for the biggest private companies will radically change the complexion of private markets, but the unicorn universe is accustomed to turnover. Looking at the top private companies of 10 years back, most have gone public. In fact, Palantir PLTR and Uber UBER are now large-cap stocks, while Xiaomi 01810 is one of China’s premier companies.

By way of comparison, five of today’s 10 largest public US companies were also in 2016’s top 10—Apple, Microsoft, Berkshire Hathaway BRK.A, Facebook (now Meta), and Amazon.com. Even as companies stay private for longer, they still see public market listings as a goal. It may take time, but others are likely to fill the void left by mega-IPOs.

How Will Mega-IPOs Affect Public Markets?

The Magnificent Few could soon enter public market equity portfolios. Index providers are figuring out how to handle the mega-IPOs, courting controversy along the way. CRSP, for its part, has long fast-tracked IPOs for benchmark inclusion in order to reflect the market in an up-to-date fashion. But it is relaxing its requirements for what percentage of a company must float publicly. SpaceX’s expected offering size of $75 billion would represent just a small fraction of its overall value.

To some, the IPOs will provide easier access to companies at the forefront of transformational new industries and technologies. SpaceX is undeniably unique, with its business lines in space infrastructure and AI. OpenAI and Anthropic are pure plays in a way that Microsoft and Alphabet are not.

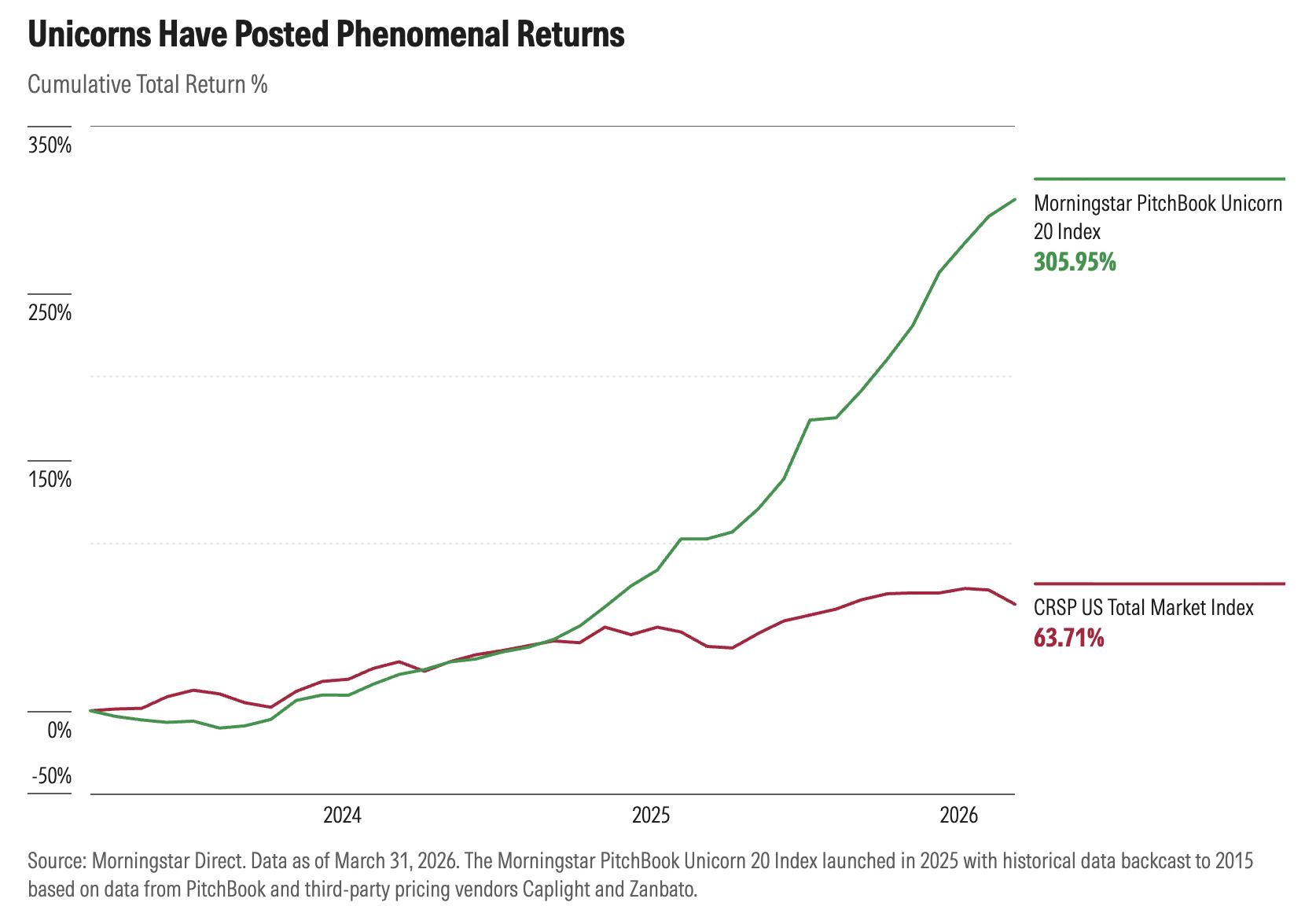

As private companies, these businesses have produced some jaw-dropping returns. The Morningstar PitchBook Unicorn 20 Index tracks the largest and most liquid unicorns using pricing from secondary trading platforms. That index has risen threefold since the first quarter of 2023, trouncing the broad US stock market.

What about their prospects as public companies? Bulls point to examples of businesses whose market values skyrocketed post-IPO. Meta’s share price has risen nearly twentyfold since going public in 2012. Palantir’s stock price is up from $13 in 2020 to more than $150 today, despite persistent charges of overvaluation.

There are plenty of counterexamples, though. IPOs are often priced to enrich private equity holders and bankers at the expense of public market investors. Consider the poor share price performance for some of 2025’s biggest IPOs, including the aforementioned Figma but also Klarna KLAR, Chime CHYM, and Navan NAVN. (CoreWeave CRWV and Circle CRCL have fared better.)

Skeptics worry the mega-IPOs reflect an AI bubble. Analysis by PitchBook researcher Harrison Rolfes noted a disconnect between valuations and revenue quality for the private AI giants, which he calls “mostly priced on promise.” He deemed Databricks, a data infrastructure company, to be of higher quality than OpenAI, despite commanding one-sixth the valuation. PitchBook’s work on SpaceX called a $1.5 trillion valuation “rich but not irrational.” Since that research was published, the valuation seems to have climbed higher. Parallels have been drawn between AI and bubbles around new technologies throughout history.

Keep the Mega-IPOs in Perspective

It’s important to remember, though, that the mega-IPOs won’t dramatically change public market complexion—at least for a while. When the companies’ values are adjusted by free float, they don’t look as big. CRSP indexes weight their constituents by float-adjusted market capitalization. At $75 billion, SpaceX would fall outside the market’s top 100 companies. Yes, free float will climb as lockup periods for private market investors expire. But during that time, investors will also weigh in on valuation.

The potential IPOs are a big deal. That’s especially true for the venture capital-backed landscape, where exits will leave a void. For public markets, IPOs mean far easier access to highly sought-after companies. Yes, there’s price risk attached to those companies. And true, their additions will contribute to the US stock market’s exposure to AI and to its technology sector concentration. But their impact should be kept in perspective. Because of limited free float, the mega-IPOs won’t be quite as mega as public companies.

Morningstar acquired the Center for Research in Security Prices in February 2026.

Also published on Morningstar.com.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.