Direct lenders in Europe feel relatively optimistic about 2023. But in an unpredictable environment it is far from clear whether managers should prepare for recession or business as usual.

“The market has seen time and time again all sorts of adversity, and I don’t see why it should collapse now,” one debt advisor said. “There are always going to be geopolitical or financial disruptions.”

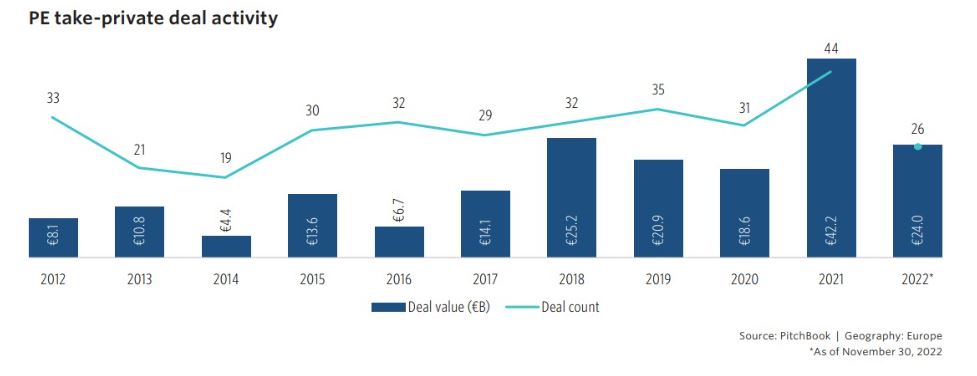

However, private lending funds and banks are both reliant on private equity for deals, and activity is likely to remain suppressed early in the year.

“It won’t be easy. Deals are scarce, and will remain so until at least 2Q23, while we are going to see companies struggling considerably as energy costs will be even higher,” one M&A lawyer said.

Heavy leverage loads also threaten some businesses as energy prices and supply chain disruptions compound the aftermath of Covid, one banker explained.

“There is €200 billion of debt that needs to be refinanced by 2025, so issuers and debt providers alike will have to come to terms with that, and I hope the context will allow us to do it,” another banker said.

As of Dec. 31, there was €64 billion of loans outstanding in the Morningstar European Leveraged Loan Index (ELLI) due to mature by the end of 2025, according to LCD data. In the US, loans outstanding in the Morningstar LSTA Leveraged Loan Index due to mature by the end of 2025 totaled $280 billion.