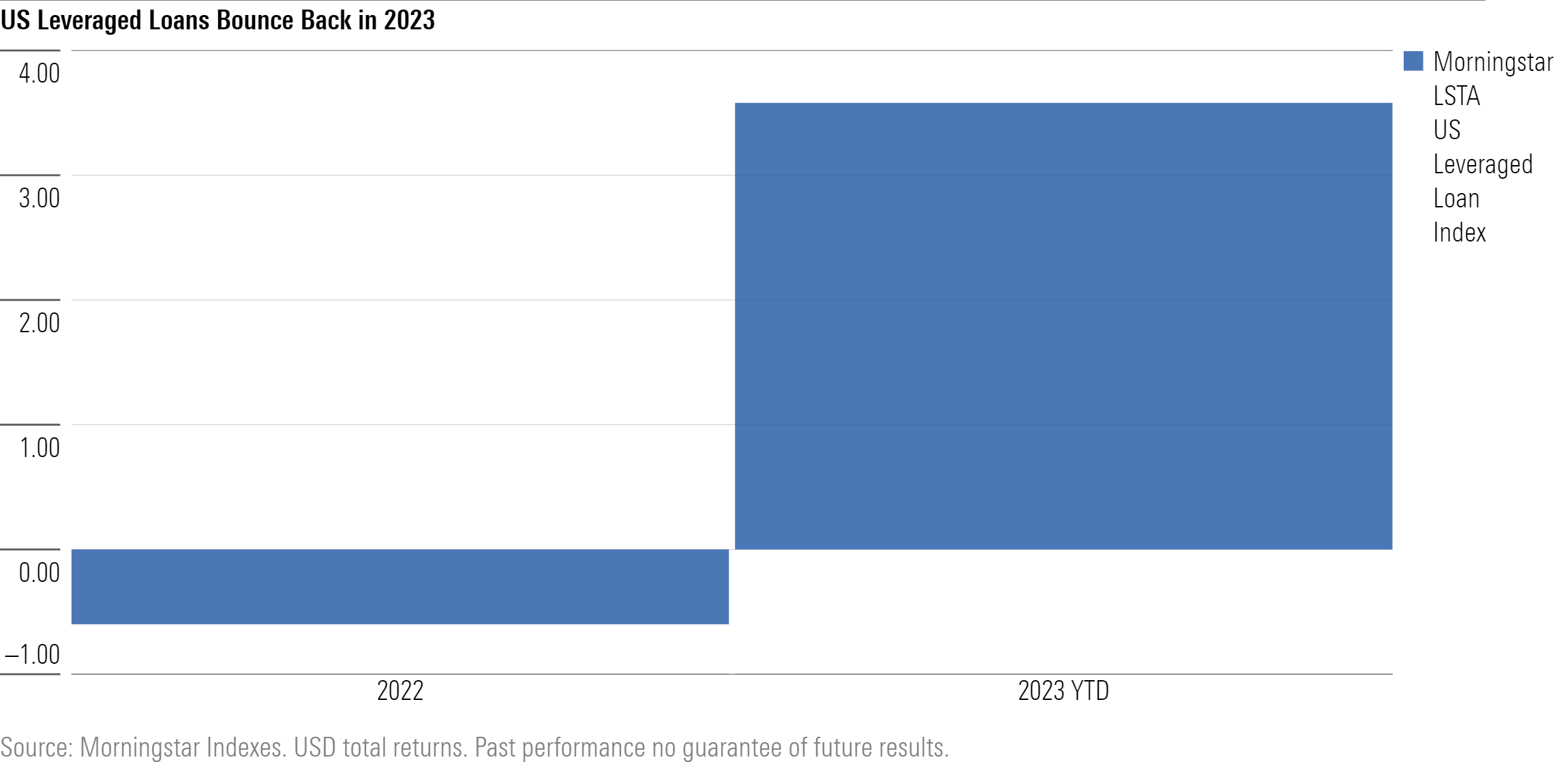

The Morningstar LSTA US Leveraged Loan Index, which measures the performance of the broad US leveraged loan market, has risen 3.58% in 2023 as of February 14. This extends its positive daily streak to 56 days, the longest stretch since January 2020, and follows a challenging 2022 in which the index lost 0.6%.

Morningstar experts see strong performance in the US leveraged loan market so far in 2023 as reflected by a recovery in average bid price and outperformance of lower rated CCC debt, which has returned more than 5.1%. This has all been buoyed by rising yields, topping 9%, and a low default rate relative to historical levels. In fact, the average bid price of the index is currently at $94.66, up from $92.44 at the start of the year.

Katie Binns, Director of Multi-Asset & Fixed Income Indexes, Morningstar:

“Investor confidence in the US leveraged loan market has returned, with leveraged loans on a growth trajectory that is slightly outpacing performance of high yield bonds year-to-date. This optimism is happening in the face of a Fed that continues to be hawkish and Tuesday’s CPI print that showed a continued elevated level of inflation well above the Fed’s 2% target. The market has a lot of time to run between now and the FOMC meeting and rate decision in late March, so we will continue to watch it closely.”

Marina Lukatsky, Global Head of Credit Research, PitchBook LCD:

“A rally in the secondary loan market has spurred opportunism as borrowers utilize the open window to chip away at looming debt maturities. Lower-rated issuers in particular have been active. Whereas refinancing volume in the fourth quarter of 2022 was predominantly from issuers in the less-risky, double-B ratings bracket, the balance has shifted in the first quarter, with single-B names taking up the bulk of the activity. In addition, private equity sponsors are testing the waters with dividend recaps, which are loans that add debt to a portfolio company, with the proceeds going back to the sponsor. Typically these types of credit emerge in a hotter, more borrower-friendly lending environment. LCD tracked four loans for this purpose from PE-backed borrowers in the last 30 days vs just two in the second half of 2022.”

©2023 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.