Major index providers ― including Morningstar― are adjusting their IPO inclusion approach, lowering free float requirements which could accelerate the timetable for index inclusion. SpaceX, Anthropic and OpenAI, notable unicorn companies expected to go public within the next year or two at historically large valuations, have created a sense of urgency among major indexes expected to track these companies.

As a result, approaches to index IPO inclusion are quickly changing, as providers rethink traditional rules for ushering in newly public companies. Why the change, why now, and what does it mean for investors?

“Companies are staying private much longer and are often coming to market with much higher market value and lower free float (i.e., shares available to public investors) than they did a couple decades ago,” according to Alex Bryan, director of Global Equity Indexes for Morningstar. “For indexes designed to closely track the overall market, it is important that we evolve our eligibility rules to keep our benchmarks relevant to new market realities.”

The CRSP Market Indexes, recently acquired by Morningstar, already have a fast-track IPO process built into their methodology, having introduced it for large caps at their initial launch and extending to small caps in 2017. On April 27, the CRSP indexes IPO inclusion process will be enhanced to introduce an alternative liquidity screen to the float requirements for larger companies with the aim of ensuring sufficient liquidity of the new entrants, while maintaining accurate representation of the investable universe.

Why should investors care? Morningstar Indexes believes that to remain representative, benchmarks should adapt as markets evolve without losing focus on transparency and accessibility. Delaying index entry for major new public market entrants may detract from the original premise of passive, index-based market exposure for investors.

“Excluding a major company from an index only based on a lower float ― a useful but imperfect measure associated with lower liquidity – can mean limiting a passive investor’s exposure to an accurate representation of the investable market,” said Alex Poukchanski, Director of Index Analytics for Morningstar Indexes.

Other market experts ask, “what’s the rush?” citing concerns around liquidity and volatility that could result from a very large company with a relatively limited market float entering the indexes too quickly after going public. Based on historical analysis of new IPOs in the CRSP mega- and mid-cap indexes, Morningstar Indexes did not see strong evidence of liquidity issues for investors.

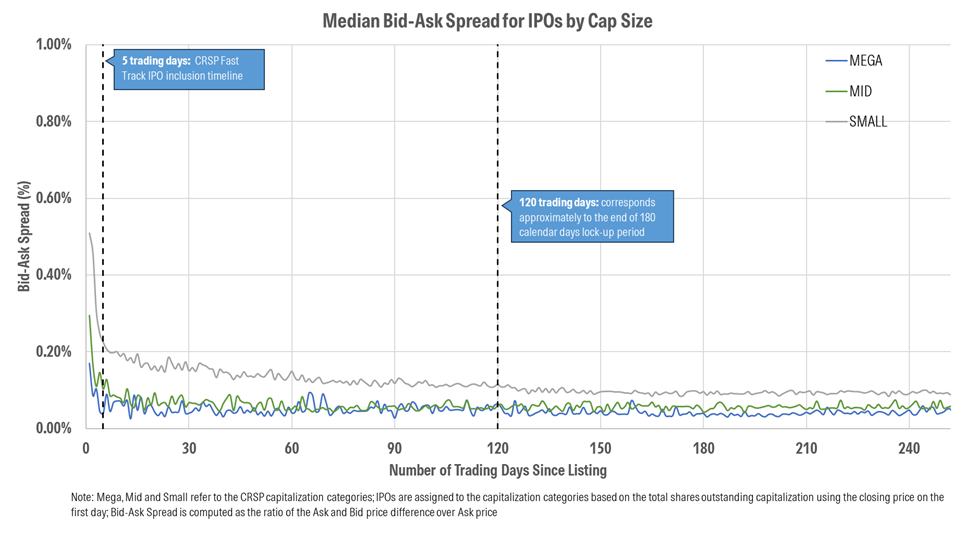

Within five days of listing, mega-, mid- and even small-cap IPOs generally have tight bid-ask spreads as to not impose high transaction costs to the investors willing to purchase them close to the listing (see the chart below). While the sample size for Mega and Mid companies is small – about 40 companies since 2013 – the chart also illustrates that larger cap companies quickly achieve liquidity, as measured by bid-ask spread, like what is expected at higher float post expiration of lock-up periods. This further illustrates the point that while float is an important measure of liquidity, so is the size of the company.

CRSP US Stock Database Suggests Mega-Cap IPOs Bid-Ask Spread Not Impacted Post-Listing

Added Rodney Comegys, CIO of Vanguard Capital Management and head of global equity, “Everything Vanguard does starts with a simple question: what’s best for investors? In our view, index funds should accurately represent the investable opportunity set of the market, and when large, liquid companies come public, it often makes sense for them to be reflected in market benchmarks as quickly as is practical. Thoughtful evolution in index inclusion standards helps ensure investors aren’t missing meaningful sources of market return. That’s why Vanguard consistently advocates for changes that strengthen market representation and ultimately improve outcomes for investors.”

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.