Although I write a lot about global investing, I tend to focus on international equities as opposed to fixed income. So, I was happy to receive an inquiry from a reader about global bonds. It concerned the merits of international fixed-income exposure in a US-based investor portfolio.

If you like your income tax-free, you can stop reading now. I’ve written about the foundational role municipal bonds play in many investor portfolios, but the US tax exemption only applies to debt issued by US states, territories, and government entities. Global bonds are for tax-sheltered accounts or investors who are otherwise less tax-sensitive.

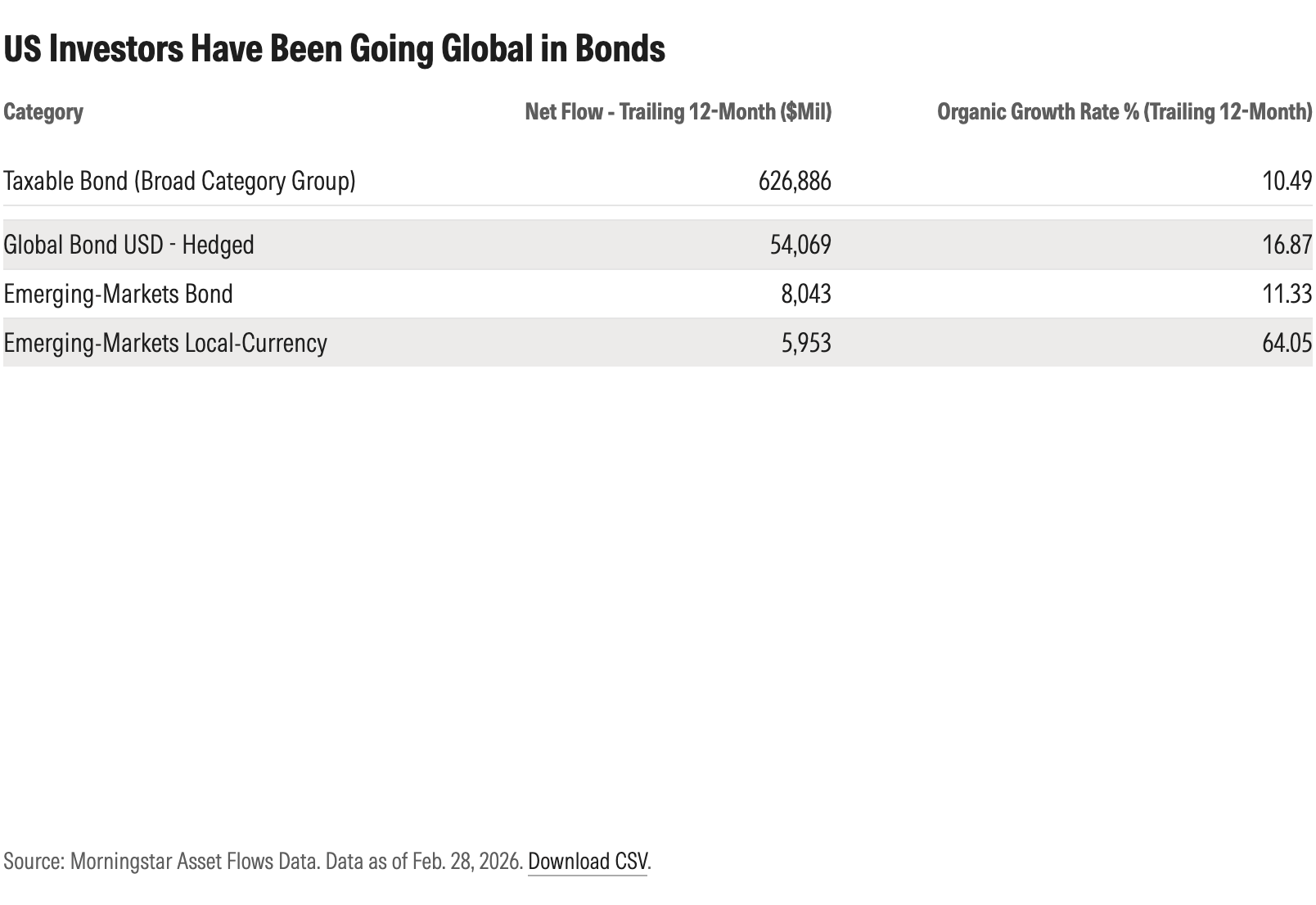

When I look at asset flows for Morningstar’s taxable-bond categories for mutual funds and exchange-traded funds sold in the US, I see emerging-markets local currency, global bond-USD hedged, and emerging-markets bond as having attracted serious inflows over the past 12 months. All three categories have grown faster than the overall taxable-bond grouping. Clearly, the reader inquiry was indicative of a broader trend that’s worth exploring.

What’s the Current Appeal of International Bonds?

Investors have been going global in bonds in part because of the “Sell America” trade. That term, which first surfaced in early 2025 when the Trump administration’s tariff policy roiled markets, is associated with a falling US dollar, rising Treasury yields, surging gold prices, and a general exodus from US assets. The panic following the “Liberation Day” tariff announcements subsided fairly quickly. But “Sell America” trended throughout 2025, mostly on US-China trade tensions, then again in early 2026 with President Donald Trump’s talk of acquiring Greenland. Clearly, investors in the US and around the globe are looking to hedge their bets by diversifying geographically.

Interestingly, the Iran war has boosted the dollar but not Treasuries. Yields on US government bonds, long perceived as a “safe haven” asset, have risen. The market may be anticipating inflation as a result of higher energy prices.

US debt and deficit fears could also be contributing. War-related expenses will only add to the US debt burden, which stands at roughly 120% of gross domestic product and seems to be on an upward trajectory. The “debasement trade” is associated with a declining dollar and rising gold prices.

It should be noted that rising government debt is not a uniquely American phenomenon. Debt concerns have contributed to recent weakness in Japanese government bonds. Since the start of the Iran war, yields on bonds issued by many governments have risen. The war’s economic consequences are clearly far-reaching.

Along with all those push factors away from the US, there’s the pull of international fixed income. My Morningstar Investment Management colleagues who specialize in asset allocation currently see opportunity in global fixed income. Developed‑market government bonds outside the US provide meaningful yield opportunities for the first time in years, they note. Rising policy rates abroad have lifted local yields. They see benefit in hedging currency exposure back to the dollar.

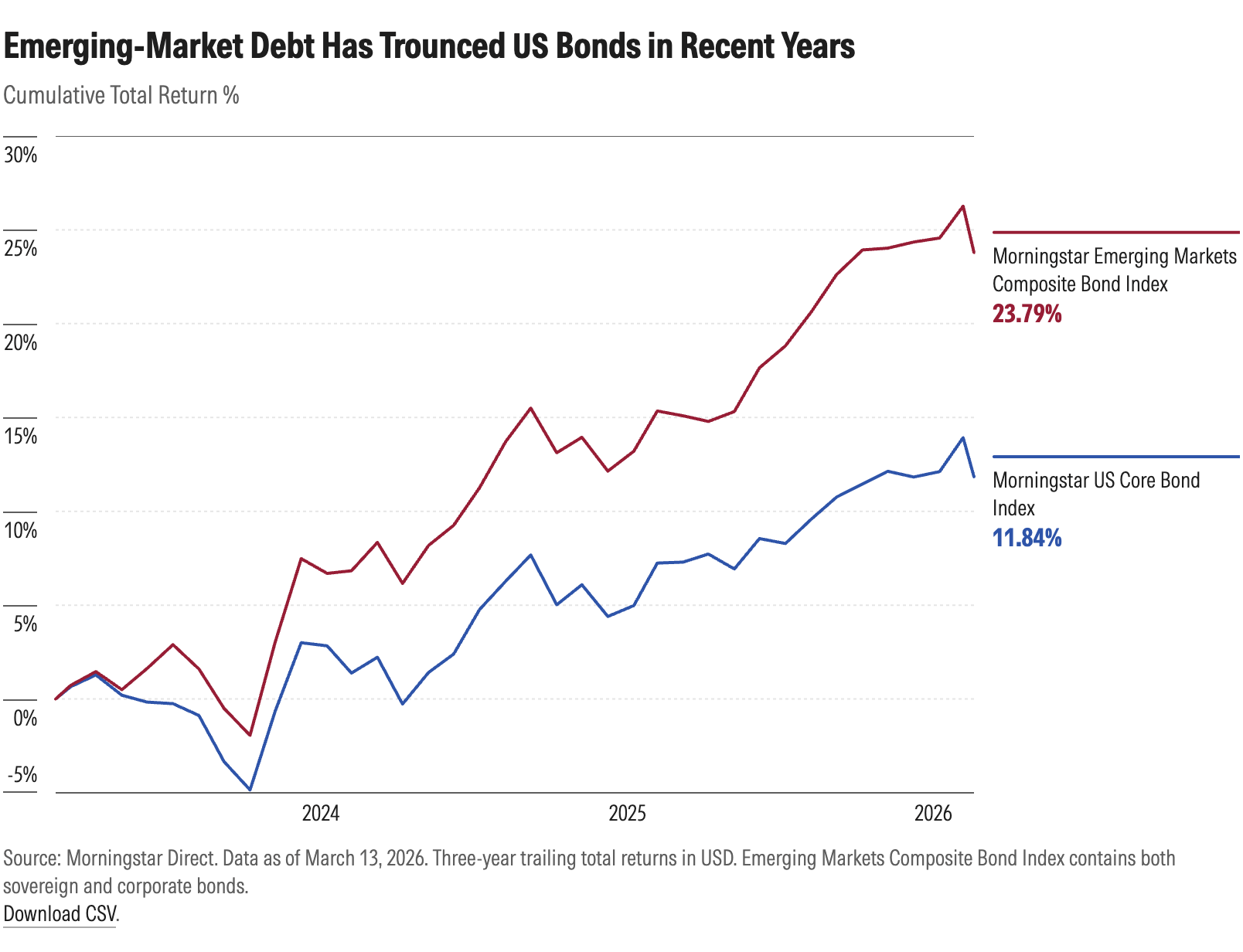

When it comes to emerging-market debt, investors have clearly been chasing strong performance in recent years. Over the past three years, the Morningstar Emerging Markets Composite Bond Index has trounced the Morningstar US Core Bond Index. Its yield of 5.5% has given it an advantage over the 4.1% yield on investment-grade US bonds. Debt issued in countries like Mexico, China, Brazil, and Saudi Arabia—both government and corporate—have performed well.

The gains for emerging-market debt in recent years owe both to the dollar’s decline and emerging economies’ improving macroeconomic positions. In a sense, roles have reversed, and developed world governments have been profligate, while emerging economies have been more disciplined. Morningstar’s 2026 Global Investment Outlook singled out local-currency emerging-market debt as an asset class with upside potential. Morningstar’s investment team is bearish on the dollar and sees currency dynamics as adding to that asset class’ appeal.

International Bonds as Part of the Toolkit

It’s common for active fixed-income managers to employ a global toolkit. As a group, they tend to have much higher success rates than stock-pickers, according to the Morningstar US Active/Passive Barometer report. Managers often allocate to non-US dollar debt and emerging-market debt, along with US Treasuries, corporate bonds, securitized credit, and bank loans. Investors who go passive with fixed income, of course, would have to make those allocation decisions on their own.

A global opportunity set allows managers to access different economic and interest rate cycles. Emerging-market debt is often targeted for its income. And currency can represent both opportunity and risk.

Yes, some investors see international bonds as a means of playing a falling dollar, but Morningstar portfolio strategist Amy Arnott says the case for currency hedging is stronger in fixed income than it is for equities. Currency fluctuations add volatility. That conflicts with bonds’ traditional role as portfolio stabilizers. For investors with US dollar expenses, foreign-currency exposure is a risk factor. Also, over the very long term, currency effects tend to come out in the wash.

Amy’s reasoning gets at fixed income’s traditional role as a portfolio stabilizer. For US investors, Treasuries have diversified stock market risk more effectively than most other fixed-income segments. Yes, there was a breakdown in diversification amid the high inflation of 2022. But during equity market selloffs in 2000, 2008, 2020, and 2025, Treasuries gained value.

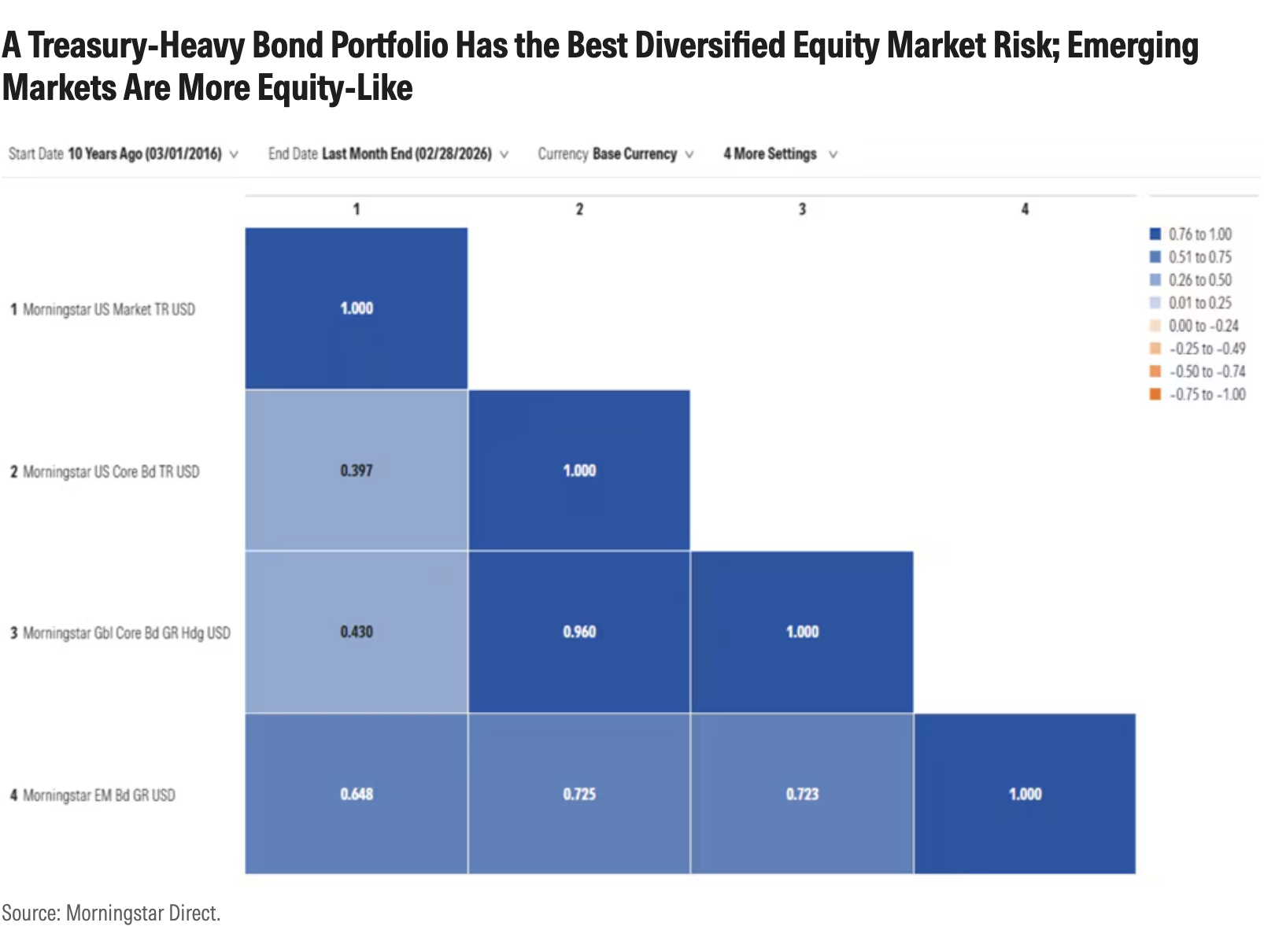

According to the correlation matrix below, the Morningstar US Core Bond Index, which is Treasury-heavy, has provided more diversification benefits than global fixed income. That said, the gap between it and the Morningstar Global Core Bond Index hedged back into the US dollar is small. Emerging-market bonds are a different story. It’s a volatile asset class, more closely correlated to equities.

International Bonds: Are They Worth Considering?

Investors holding an active bond strategy may already be getting global fixed-income exposure. If you own a fund in the intermediate core bond, intermediate core-plus bond, or multisector bond categories, non-US bonds may be part of its toolkit. There’s appeal in letting a professional management team make those allocation decisions. Passive investors who hold only a core US bond strategy might consider globalizing—either for tactical reasons or as part of a strategic allocation. Non-US bonds can contribute both income and total return to a portfolio. See Morningstar Manager Research’s Medalist Bond Funds for some good options.

Are you going global in fixed income, or thinking about it? Let me know at: dan.lefkovitz@morningstar.com. I read all my emails, even if I can’t reply to them all.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.