“Stocks for the long run.” It’s not just the title of a seminal book, but also an investment axiom. The stock market is widely seen as the surest path to building wealth and meeting long-term goals. Stock-heavy investments have even become the default option in many retirement plans.

Yet, equity investing hasn’t always been mainstream. And stocks aren’t a surefire means of building wealth. While the US stock market in aggregate has returned more than 10% per year over the past 100 years, most individual stocks don’t outperform cash. That’s the stunning conclusion reached by Hendrik Bessembinder of Arizona State University. His research is hard to reconcile with today’s investing orthodoxy.

I’m excited to interview Professor Bessembinder at this year’s Morningstar Investment Conference in Chicago. I’ll be joined by my colleague Alex Poukchanski, who came over to Morningstar as part of our February 2026 acquisition of the Center for Research in Security Pricing, a former affiliate of the University of Chicago. Bessembinder conducted his research using CRSP data. The history of that database, and Bessembinder’s research with it, are both worth considering as investors contemplate the future of stocks.

CRSP’s Contribution: Establishing Total Stock Market Return

CRSP was created at the University of Chicago in 1960 with an initial grant from Merrill Lynch. Professors Lawrence Fisher and James Lorie were tasked with developing a database of US stock returns. The brokerage house wanted to see the case made for equity investing.

In 1960, investors were just a generation removed from the Great Depression. Many had personal memories of the stock market crash of 1929, and many more belonged to families affected by the fallout. Stocks were widely distrusted.

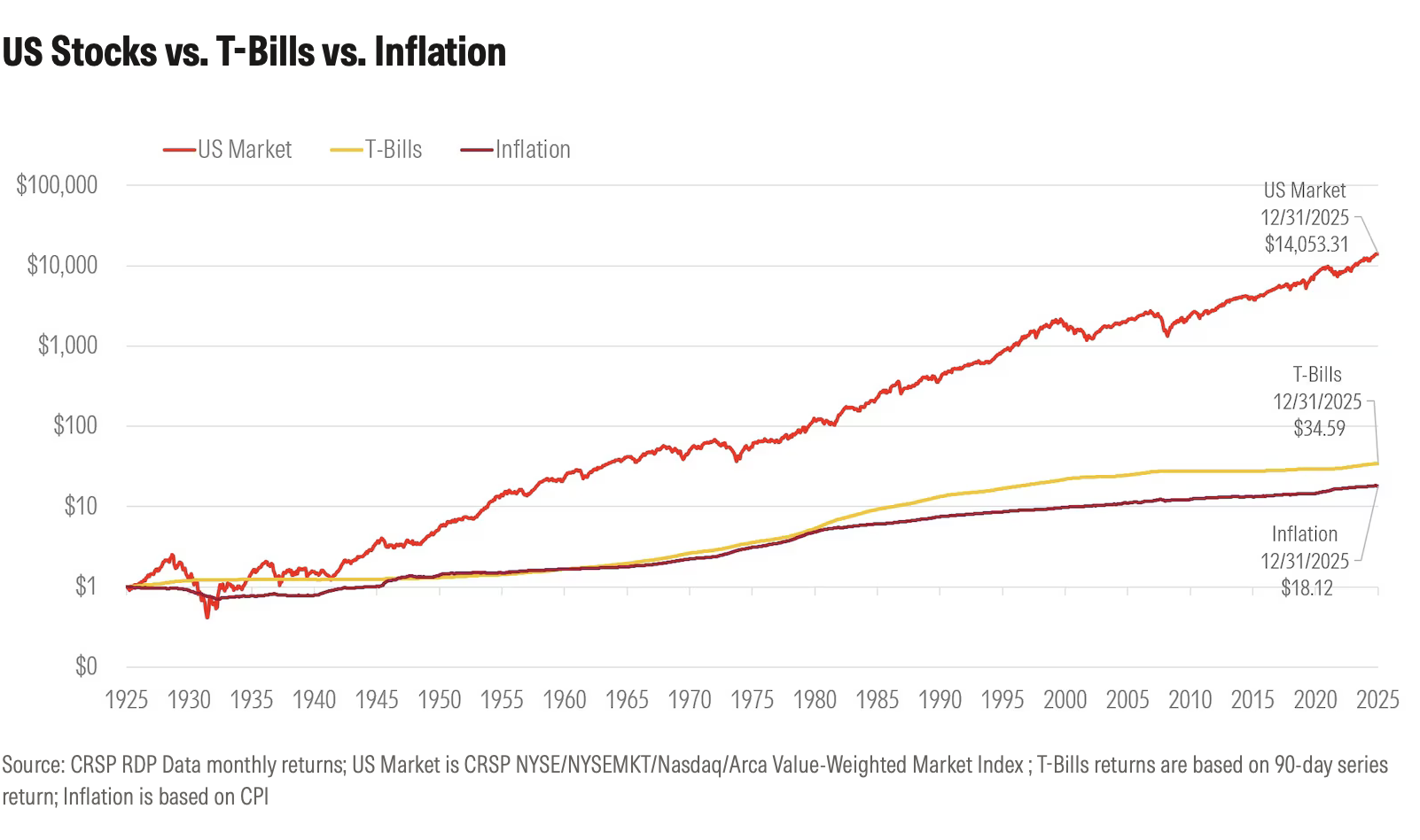

It took Fisher and Lorie three and a half years and miles of magnetic tape to assemble data and crunch numbers. Their 1964 paper, Rates of Return on Investments in Common Stocks, was groundbreaking. It established a “total market return” by equally weighting all the stocks listed on the New York Stock Exchange between 1926 and 1960. That composite returned roughly 9% per year over a 35-year period that included the crash and difficult years during the Great Depression. Stock returns far surpassed Treasury bills.

CRSP’s database now goes back a century. Updated through the end of 2025, it shows an average annual return over the past 100 years of 10% for a market-capitalization-weighted aggregate of US-listed stocks. That’s before inflation and taxes.

Bessembinder Questions Individual Stock Return

Given that history, Do Stocks Outperform Treasury Bills?, published by Bessembinder in 2017, came as quite a shock. He found that most stocks actually fail to beat Treasury bills over their lifetimes. A small number of superstar stocks are responsible for the vast majority of the overall market return. In short: Most stocks stink.

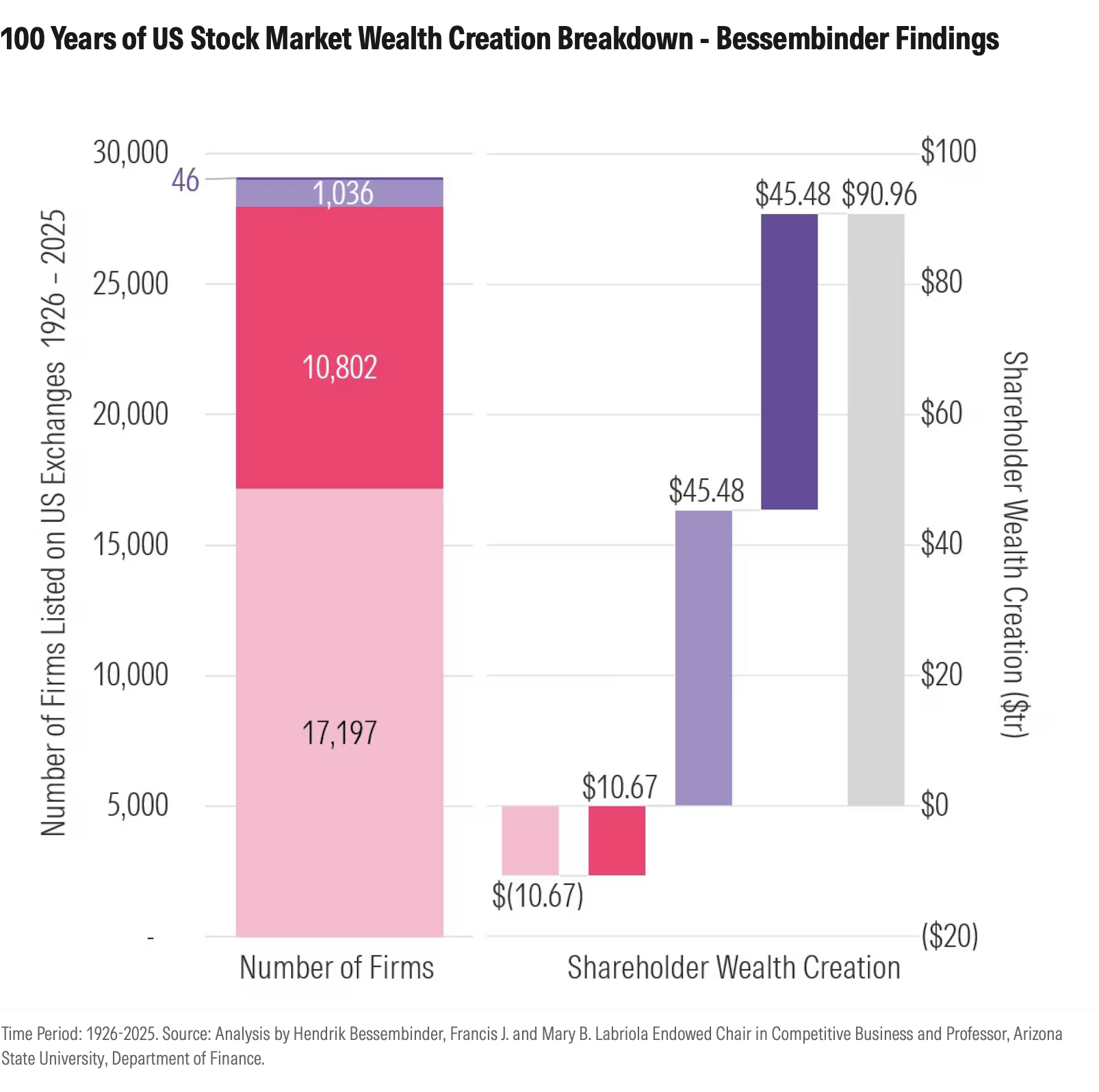

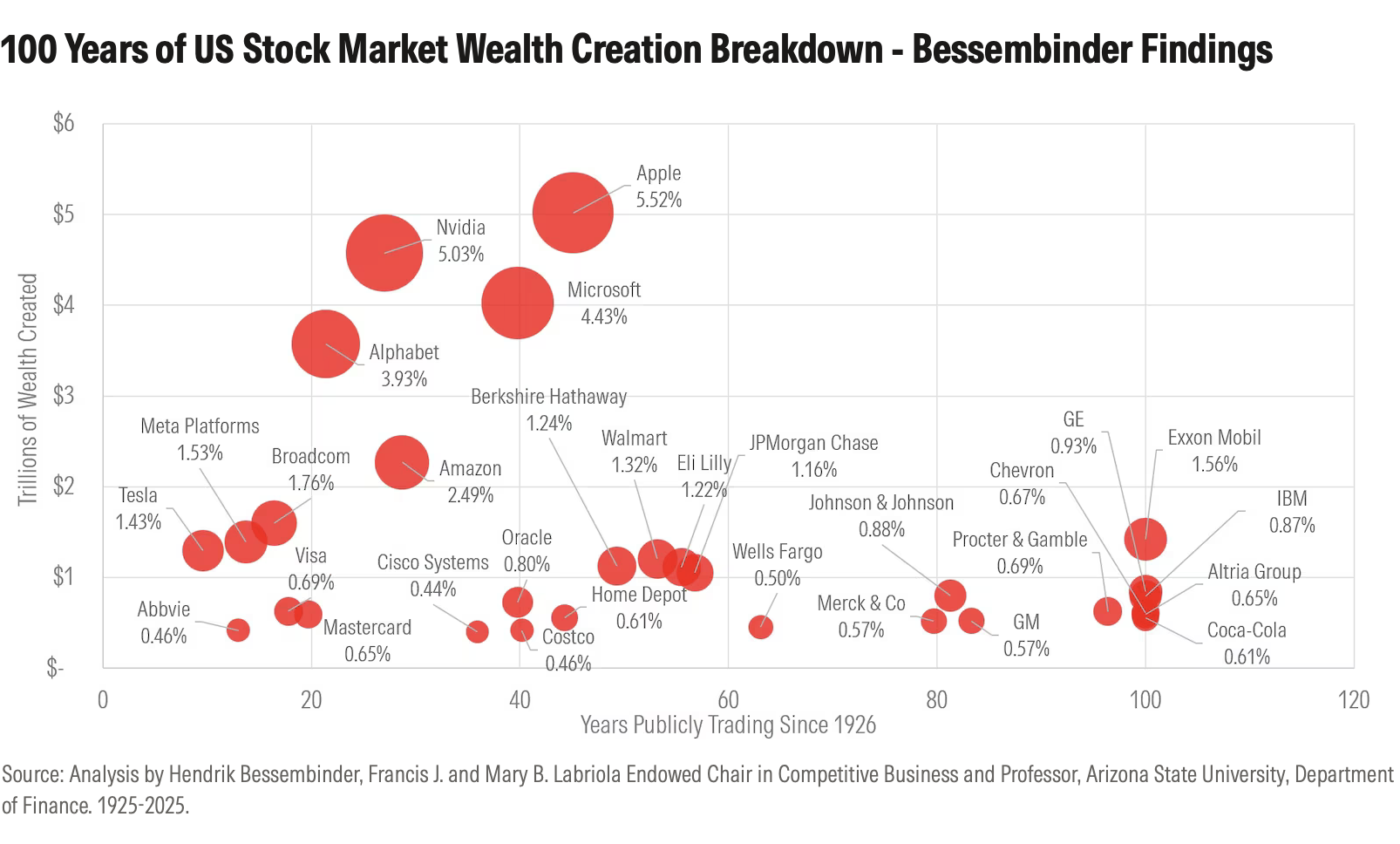

Earlier this year, Bessembinder updated his research in One Hundred Years in the U.S. Stock Markets. Studying roughly 30,000 US stocks between 1926 and 2025, he found that less than half posted positive returns and just 41.17% outperformed the US Treasury bill. Just 46 stocks accounted for half the $91 trillion of wealth created. That concentration of wealth creation had increased since his original study. In 2017, he found that 89 stocks accounted for half the wealth created.

What Are the Takeaways From Bessembinder’s Research?

Alex and I have lots of questions for Bessembinder. Top of mind for all the stock-pickers out there: What are the common attributes of superstar stocks? The list of biggest wealth creators includes young companies like Tesla TSLA, Alphabet GOOGL, and Nvidia NVDA, as well as some stalwarts, such as Coca-Cola KO, General Motors GM, and Johnson & Johnson JNJ. Naturally, we’ll want to know if there’s any way of identifying superstars in advance. Do they share fundamental characteristics? Do they tend to cluster in certain sectors, sizes, or style segments?

We’ll also ask Bessembinder if his research is a better argument for active or passive management, highly concentrated or broadly diversified portfolios. Some might say a selective approach is the best way to avoid the stinkers and tilt toward wealth creators. Fans of passive management would invoke Vanguard founder Jack Bogle: “Don’t look for the needle in the haystack. Just buy the haystack!”

If you’re coming to the Morningstar Investment Conference, please stop by and say hi. I love to meet readers in person. And Professor Bessembinder gives autographs.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.