The Morningstar Wide Moat Focus Index targets undervalued US stocks with wide economic moat ratings, as determined by Morningstar equity analysts.

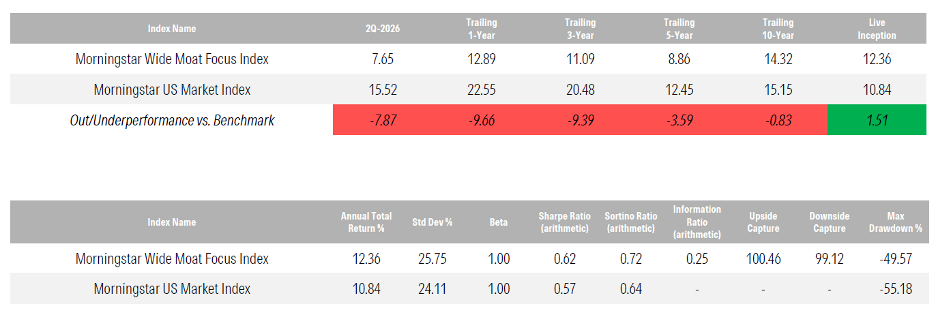

The second quarter of 2026 was a disappointing period for the index. The index delivered only a 7.65% total return as its benchmark, the Morningstar US Market Index, rose 15.52% in the same period. This amounted to 787 basis points of underperformance, one of the most challenging quarters in the index’s lengthy history.

Performance & Risk Metrics

Live Inception: 2/14/2007 | Data as of: 6/30/2026 | Benchmark: Morningstar US Market Index | Source: Morningstar Direct | Data Frequency: Daily | All performance data reflects USD total returns | Indexes are unmanaged and not available for direct investment.

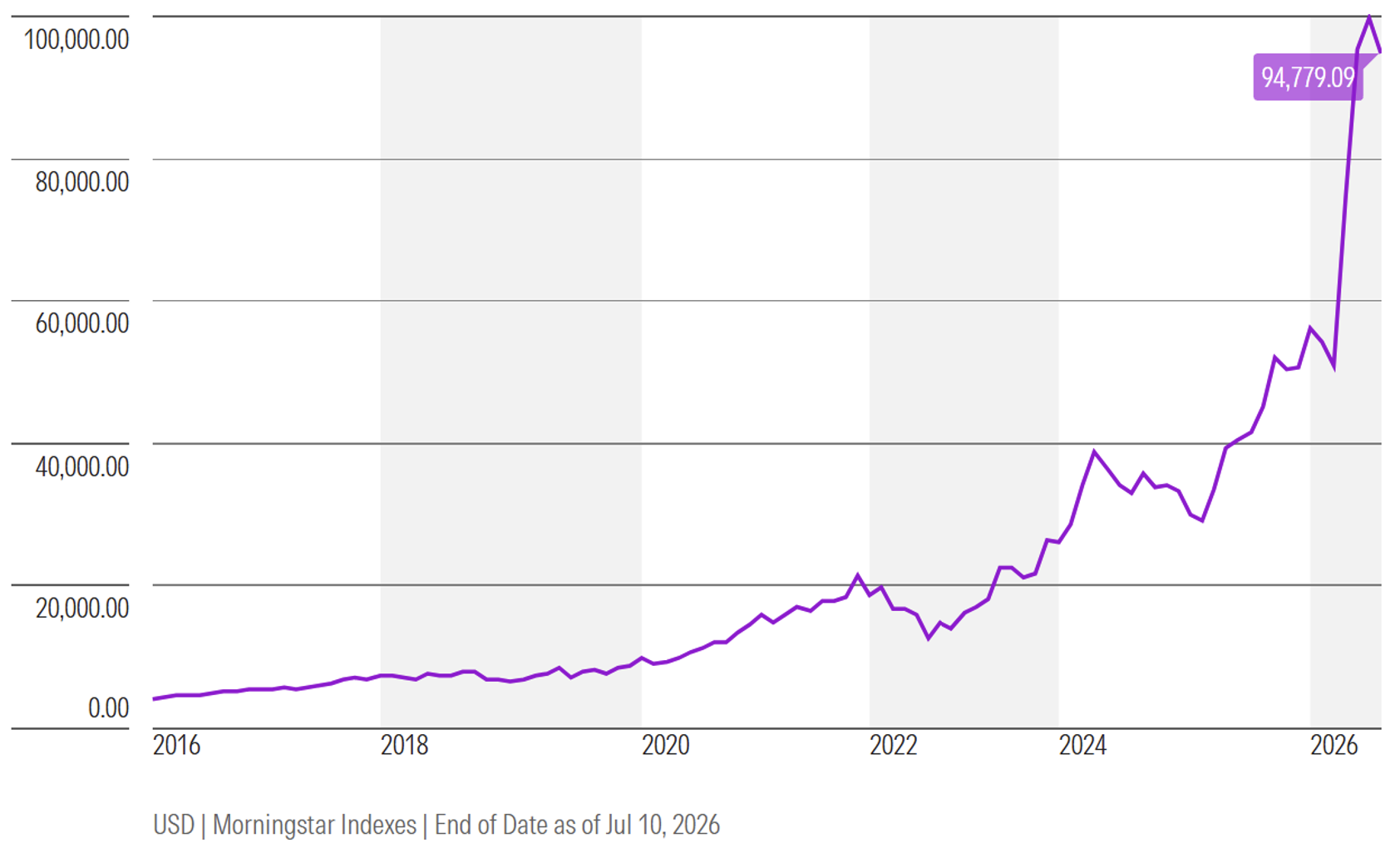

At the industry level, one of the biggest market trends was the historic run in the semiconductors industry in the second quarter, as the Morningstar North America Semiconductors Index rose 95%. The index had a roughly 10% exposure to semiconductors versus 15% in the benchmark.

Stock selection within the semiconductors industry was modestly negative as non-wide moat names were among the biggest relative winners in the second quarter. The Morningstar Wide Moat Focus Index’s omission of no-moat Micron, narrow-moat AMD, and no-moat Intel proved adverse. The share price for each company more than doubled in the second quarter, and their omission detracted from excess returns by 288 basis points.

Morningstar North America Semiconductors Index Performance Since 2016

Source: Morningstar Direct

On the bright side, the Morningstar Wide Moat Focus Index benefitted from favorable selection effect in the software sector during the quarter. In March, AI disruption fears, spurred by the release of Anthropic’s Claude Cowork and OpenAI’s Codex, inspired us to reevaluate the economic moat ratings of 132 companies across our global coverage. This work led us to downgrade several stocks to narrow moat ratings, which led to their removal from the index in mid-March and mid-June. At the same time, we retained wide moat ratings for several other firms that we believe will hold up well in the age of AI.

The index has been overweight software year-to-date, and the industry has struggled immensely from a return perspective. However, highly favorable stock selection within the software industry more than offset the headwinds from this industry overweight.

The three best-performing holdings in the quarter were Fortinet, Datadog, and Palo Alto Networks. All three of these names had been subject to what we viewed as an unjustified sell-off amid the “SaaSpocalypse,” and their recent recoveries validated this view. Stock selection within software was also aided by minimizing exposure to some of the biggest losers, such as Adobe, Workday, Salesforce, ServiceNow, and Oracle, where we recently booked recent economic moat downgrades.

Another significant US stock market trend in the second quarter was a reduction in Crude oil prices from $101 on March 31 to $69.50 on June 30, thanks to improved relations between the US and Iran as of the end of the second quarter. The index’s underweight position in the energy sector contributed to excess returns by 114 basis points.

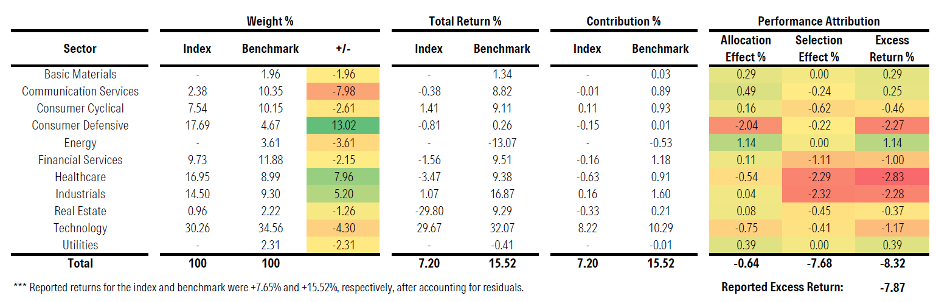

Looking at the Morningstar Wide Moat Focus Index, like the first quarter, the index primarily suffered from unfavorable stock selection, as sector weightings driving only a modest headwind. The index held some notable underperformers in the healthcare sector, with Zoetis, GE Healthcare, and Thermo Fisher each suffering a sharp sell-off after reporting earnings. Stock selection in the Industrials sector was also poor during the second quarter, as the sector rose 17% within the benchmark but only 1% within the portfolio. Huntington Ingalls and Northrop Grumman were two of the biggest detractors.

Sector weightings provided only a modest headwind, weighing on excess returns by 64 basis points. The index remains overweight the Consumer Defensive sector, which failed to rally with the rest of the US market in the second quarter. Partially offsetting this headwind was the index’s underweight exposure to the Energy sector, which also underperformed as oil prices moderated.

Time Period: 4/1/2026 – 6/30/2026 | Benchmark: Morningstar US Market Index | Source: Morningstar Direct | All performance data reflects USD total returns | Indexes are unmanaged and not available for direct investment.

Finally, despite the index’s second quarter performance having been disappointing overall, performance was most detrimental from the start of the quarter through mid-May. More recently, the index has outperformed its benchmark by +507 basis points from May 15 to July 10. Favorable stock selection in Technology (including software winners) and Consumer Defensive, plus avoidance of the underperforming Communications Services sector, have contributed to this improved relative performance.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.