The Takeaway

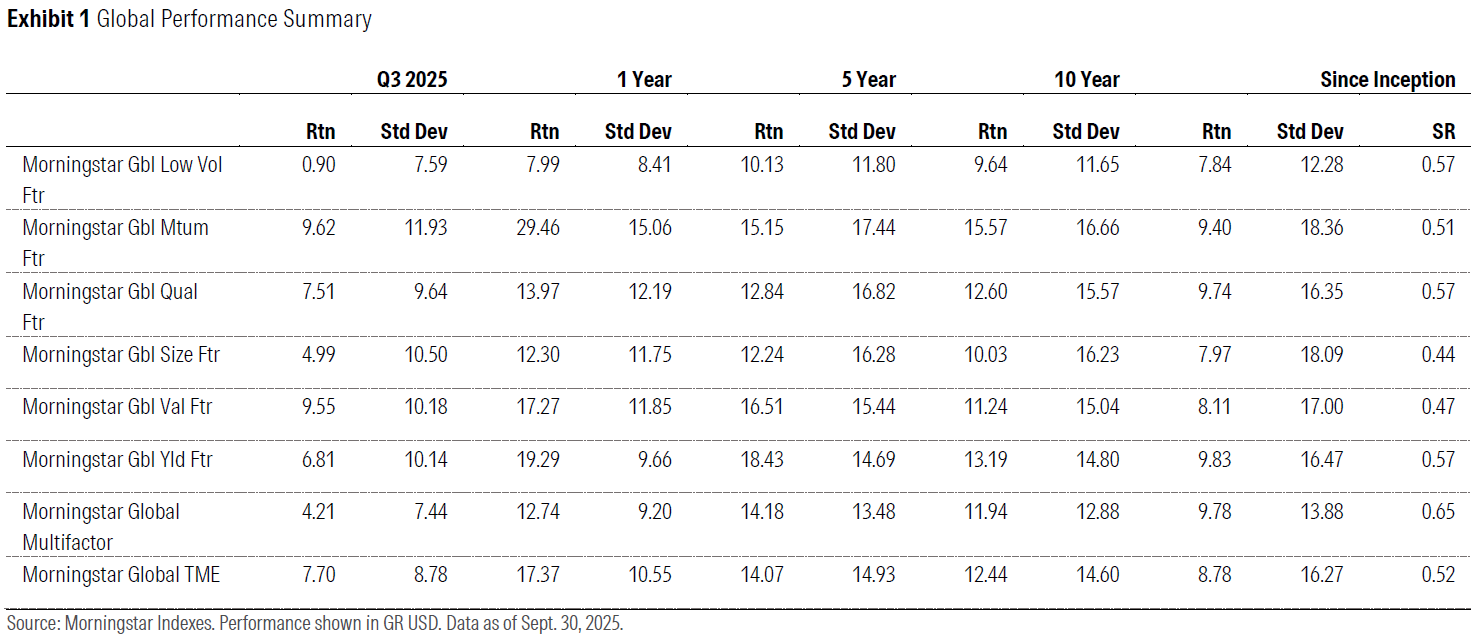

Consistent with the trend observed in the second quarter of 2025, momentum was the top-performing factor globally, while low volatility was the worst-performing.

Consistent with the trend observed in the second quarter of 2025, momentum was the top-performing factor globally, while low volatility was the worst-performing.

The value factor performed much better in the third quarter than it did in the second, ranking as the second-best-performing factor behind momentum globally and as the best-performing in developed markets outside the US.

The value factor performed much better in the third quarter than it did in the second, ranking as the second-best-performing factor behind momentum globally and as the best-performing in developed markets outside the US.

Factors are complementary and offer strong diversification benefits when combined in a portfolio.

Factors are complementary and offer strong diversification benefits when combined in a portfolio.

In a continuation of the trend from the second quarter, momentum was the top-performing factor globally in the third quarter, while low volatility remained at the bottom of the rankings. The value factor performed considerably better than it had in the second quarter, finishing the third quarter in second place, just slightly behind momentum. It had previously finished second-to-last.

This joint strong performance of value and momentum is somewhat unusual as the market-relative performance of these two factors has tended to be negatively correlated. Conditions, including low market volatility and an upward-trending market, were conducive to short-term performance persistence, the foundation of the momentum factor. In contrast, the value factor tends to benefit from mean-reversion, which is less prevalent in strong-trending markets.

While conditions were more favorable for momentum, the Morningstar Global Value Factor Index posted strong performance, buoyed by strong intrasector stock exposure, particularly within the healthcare, financial services, and consumer defensive sectors. These included overweighting companies such as Johnson & Johnson, JPMorgan Chase, and Altria. The value index's overweighting of Alphabet also helped. Because sector tilts are tightly constrained relative to the parent benchmark, sector allocation did not have a strong impact on the value index's market-relative performance.

The Morningstar Global Momentum Factor Index benefited from strong stock exposure within the consumer cyclical and financial-services sectors, such as overweighting Tesla. Sector tilts relative to the parent benchmark (the Morningstar Global Target Market Exposure Index) did not significantly impact performance.

©2025 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.