The Morningstar Wide Moat Focus Index represents a basket of undervalued US stocks with wide economic moat ratings, as determined by Morningstar equity analysts. The index methodology typically leads to notable overweight and underweight positions as it pertains to sectors and themes.

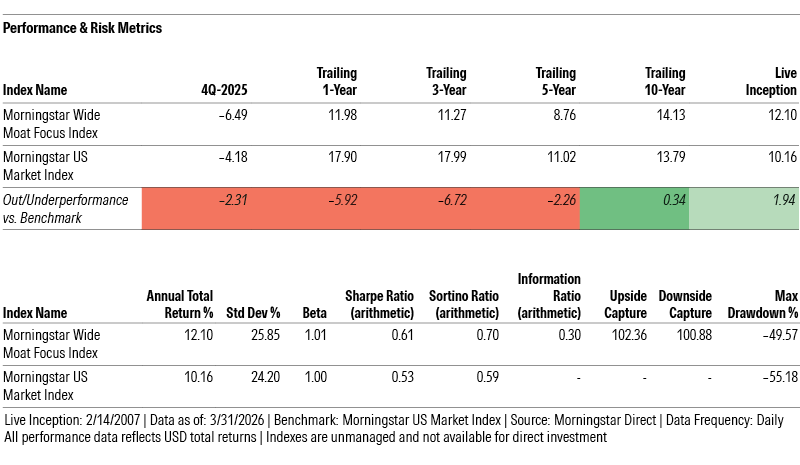

The first quarter of 2026 was an eventful, but disappointing, one for the Index, most notably due to the sharp selloff in software stocks, coined as the “SaaSpocalypse” for Software-as-a-Service companies. The Morningstar Wide Moat Focus Index was down -6.49% in the first quarter, -231 basis points worse than its benchmark, the Morningstar US Market Index, which lost -4.18%.

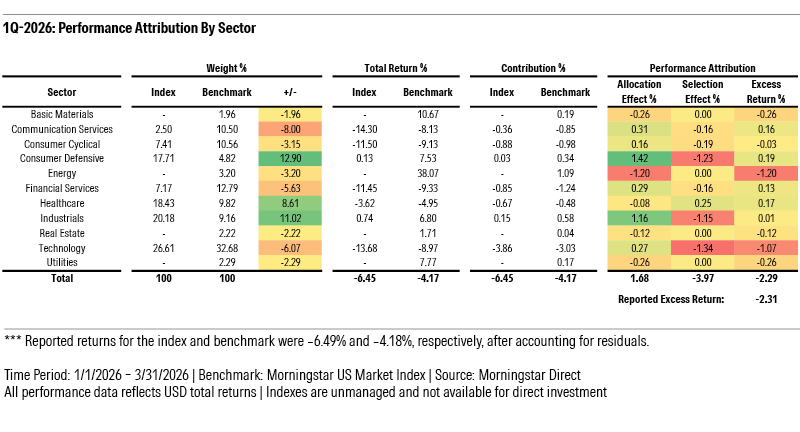

The index mainly suffered from unfavorable stock selection. The biggest drag came from the Technology sector as many software stocks traded sharply lower amid AI disruption fears. The release of Anthropic’s Claude Cowork in January 2026 triggered the rise of Agentic AI, as AI tools are now able to perform multi-step, complex coding projects. Leading software firms have been investing in AI, but agents from frontier AI leaders like Anthropic and OpenAI might disrupt large incumbents, putting their previously steady SaaS business models at risk.

Morningstar constantly assesses our economic moat ratings, and these AI fears inspired us to reevaluate the economic moat ratings of 132 companies across our global coverage. In early March, several US-based software stocks held within the Wide Moat Focus Index were downgraded to narrow moat ratings, such as Adobe, Salesforce, ServiceNow, and Workday. These names were four of the biggest detractors to Index performance in the first quarter.

On the other hand, we don’t view all software companies as AI losers. Many wide moat firms exist in software, as we believe certain companies will still thrive. Further, business fundamentals, such as revenue growth and net retention rates, have been largely undisturbed to date. Our moat ratings are forward-looking, so past performance does not preclude future AI disruption. Accordingly many wide moat-rated software companies that we reviewed retained their wide economic moat ratings.

Outside of software, being overweight the Consumer Defensive and Industrial sectors proved favorable in the first quarter. However, unfavorable stock selection within these sectors negated most of these benefits.

Finally, the Wide Moat Focus Index suffered having no exposure to the Energy sector. Exceedingly few Energy companies have a wide economic moat rating, thanks to the commoditized nature of the sector. However, the US-Iran conflict led to a spike in oil prices, which was good for Energy names held within the broader market index, but had no positive effect on the Wide Moat Focus Index.

Looking ahead across the various sectors, Technology remains the largest sector position within the Wide Moat Focus Index at 28% as of March 31, on par with the broader Morningstar US Market Index. The three primary overweight sectors are comparable with a quarter ago -- Healthcare, Industrials, and Consumer Defensive.

The Healthcare sector was one of the best performing sectors in the first quarter, driving +20 basis points of outperformance, thanks to favorable stock selection. We still see opportunities in medical devices companies like GE Healthcare Technologies, Zimmer Biomet Holdings, Thermo Fisher Scientific, and West Pharmaceutical Services. We also view Veeva Systems, a healthcare software company, as a firm that is well positioned to generate excess returns on capital in the age of AI. Veeva serves a highly regulated industry where the workflows are complex, industry-specific, and require domain expertise and regulatory backed adoption.

The Morningstar Wide Moat Focus Index’s exposure to Industrials, 18.7% versus 10.5% for the benchmark, drove +110 basis points of outperformance. However, unfavorable stock selection within the Industrials sector negated this weighting benefit by -120 basis points. Masco remains one of our top picks, as we believe that the performance of housing-related stocks will transcend the negative investor sentiment that has been plaguing them. Additionally, we see upside for certain defense companies like Huntington Ingalls Industries, Northrop Grumman, and Boeing as demand for their specialized products remains robust amid heightened geopolitical tensions and accelerating defense procurement spending.

In Consumer Defensive, the index had an 18.0% weighting versus 5.3% for the benchmark. This positioning contributed +141 basis points of outperformance. Again, however, unfavorable stock selection negated this weighting benefit to the tune of -126 basis points. We still see “affordability” as an issue for many consumers that may prompt trade down to lower-priced private-label products rather than pay higher prices for branded leaders. We anticipate that innovation and tactical marketing can help branded CPG manufacturers and retailers combat this dynamic. In turn, we still view certain names as cheap, such as Mondelez International, Clorox, Hershey, and PepsiCo.

We still see “affordability” as an issue for many consumers that may trade down to generic products rather than pay higher process for branded leaders. We still believe that R&D innovation and tactical marketing can help CPG leaders and retailers combat this dynamic. In turn, we still view certain names as cheap, such as Mondelez International, Clorox, Hershey, and PepsiCo.

©2026 Morningstar. All Rights Reserved. The information, data, analyses and opinions contained herein (1) include the proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Morningstar has not given its consent to be deemed an "expert" under the federal Securities Act of 1933. Except as otherwise required by law, Morningstar is not responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use. References to specific securities or other investment options should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Past performance does not guarantee future results. Before making any investment decision, consider if the investment is suitable for you by referencing your own financial position, investment objectives, and risk profile. Always consult with your financial advisor before investing.

Indexes are unmanaged and not available for direct investment.

Morningstar indexes are created and maintained by Morningstar, Inc. Morningstar® is a registered trademark of Morningstar, Inc.